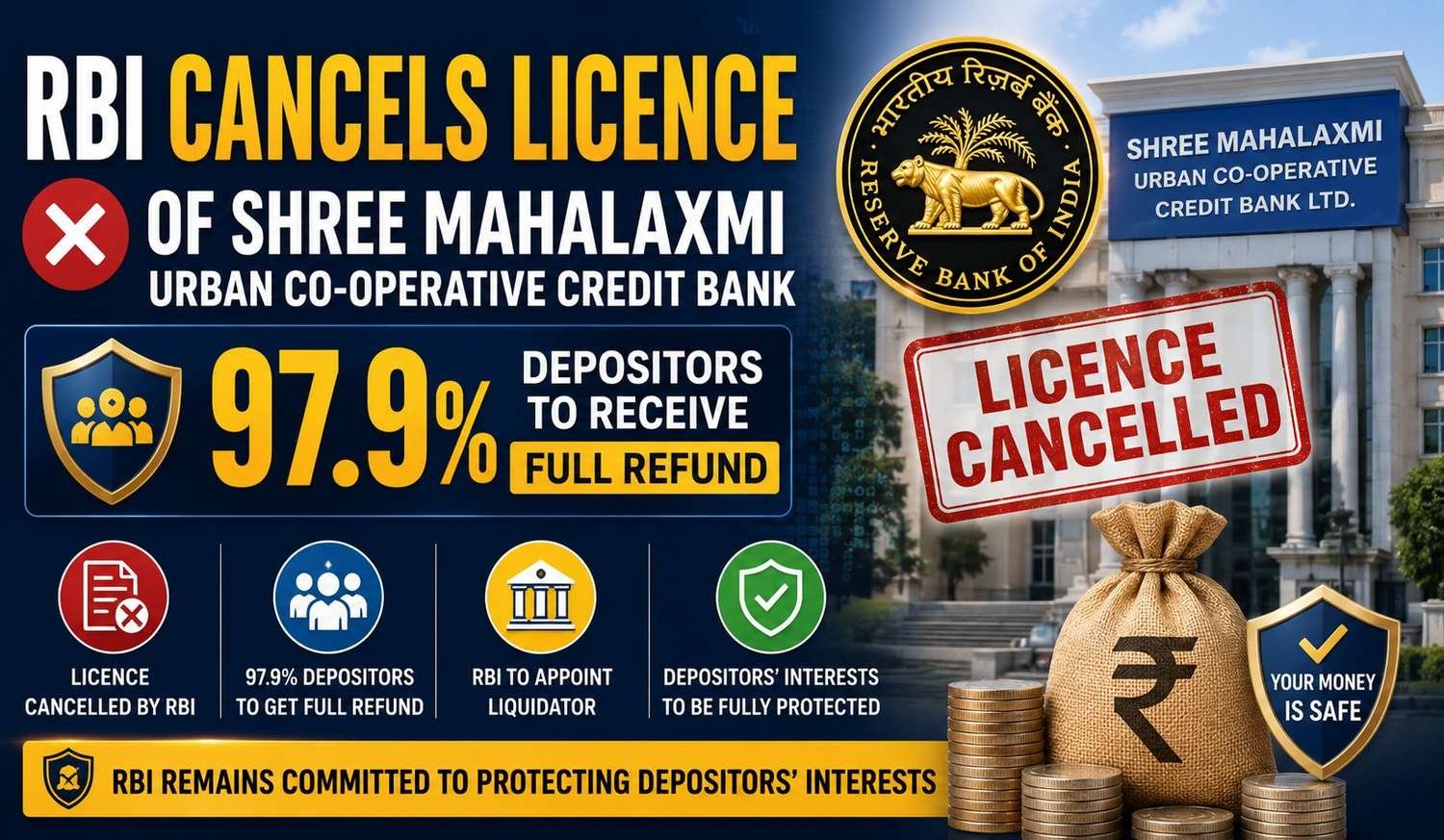

- The Reserve Bank of India (RBI) has cancelled the banking licence of Karnataka-based Shree Mahalaxmi Urban Co-operative Credit Bank, citing its deteriorating financial position and inability to comply with key regulatory requirements.

- The decision marks another significant regulatory intervention by the central bank aimed at protecting depositors and maintaining stability in the co-operative banking sector.

Why Did RBI Cancel the Licence?

According to the RBI, the bank no longer possesses adequate capital and earning prospects required to continue banking operations.

The central bank stated that the co-operative bank failed to comply with certain provisions of the Banking Regulation Act, 1949, making its continued operation unsustainable.

The RBI further noted that:

- The bank lacks sufficient capital reserves.

- It has weak earning potential.

- Its financial position has significantly deteriorated.

- It may be unable to repay all depositors in full.

As a result, allowing the bank to continue operations would be detrimental to the interests of depositors.

Bank Ordered to Stop Banking Operations

Following the cancellation of its licence, Shree Mahalaxmi Urban Co-operative Credit Bank, located in Gokak, Karnataka, has been prohibited from carrying out banking activities.

Effective immediately, the bank can no longer:

- Accept deposits from customers

- Repay deposits

- Conduct normal banking transactions

- Carry out any banking business permitted under its licence

The RBI’s order came into effect on June 18, 2026.

Registrar Asked to Wind Up the Bank

The RBI has requested the Registrar of Co-operative Societies, Karnataka, to initiate the winding-up process.

The Registrar has been advised to:

- Issue an official winding-up order

- Appoint a liquidator

- Oversee the liquidation process

- Facilitate depositor claims and settlements

The liquidator will be responsible for managing the bank’s remaining assets and liabilities.

Major Relief for Depositors

- Despite the closure, depositors have received significant reassurance from the RBI.

- The central bank stated that approximately 97.9 percent of depositors are expected to receive the full amount of their deposits through the Deposit Insurance and Credit Guarantee Corporation (DICGC).

- This means that nearly all eligible depositors will be protected under India’s deposit insurance framework.

What is DICGC?

- The Deposit Insurance and Credit Guarantee Corporation (DICGC) is a wholly owned subsidiary of the Reserve Bank of India.

- Its primary role is to provide insurance protection to bank depositors in the event of a bank failure or liquidation.

- Currently, DICGC provides deposit insurance coverage of up to ₹5 lakh per depositor per bank, including both principal and accrued interest.

- This insurance applies to Savings accounts, Current accounts, Fixed deposits and Recurring deposits.

- The scheme serves as an important safeguard for small depositors.

Why RBI Takes Such Actions

- The RBI regularly monitors the financial health of banks and co-operative institutions to ensure depositor safety.

- When a bank becomes financially weak and fails to meet regulatory norms, the central bank may take corrective action, including Imposing restrictions, Issuing directions, Facilitating mergers, Cancelling licences and Initiating liquidation.

- Such measures are intended to protect public confidence in the banking system.

Impact on Customers

- Customers of Shree Mahalaxmi Urban Co-operative Credit Bank may experience temporary inconvenience as the liquidation process unfolds.

- However, the RBI’s assurance regarding DICGC coverage provides substantial relief to most depositors.

- Eligible customers can expect reimbursement of insured deposits through the established DICGC claim process after the liquidation proceedings commence.

Conclusion

- The RBI’s decision to cancel the licence of Shree Mahalaxmi Urban Co-operative Credit Bank reflects its commitment to safeguarding depositor interests and ensuring financial stability.

- While the closure highlights the challenges faced by some co-operative banks, the availability of DICGC insurance ensures that the vast majority of depositors will recover their funds.

- With approximately 97.9 percent of customers expected to receive their deposits in full, the impact on retail depositors is likely to remain limited despite the bank’s closure.