The Reserve Bank of India (RBI) is undergoing a major shift in its regulatory approach, moving towards frequent enforcement actions with smaller penalties instead of imposing large one-time fines.

This trend reflects a structural transformation in supervision, where the focus is on continuous compliance monitoring rather than occasional punitive action.

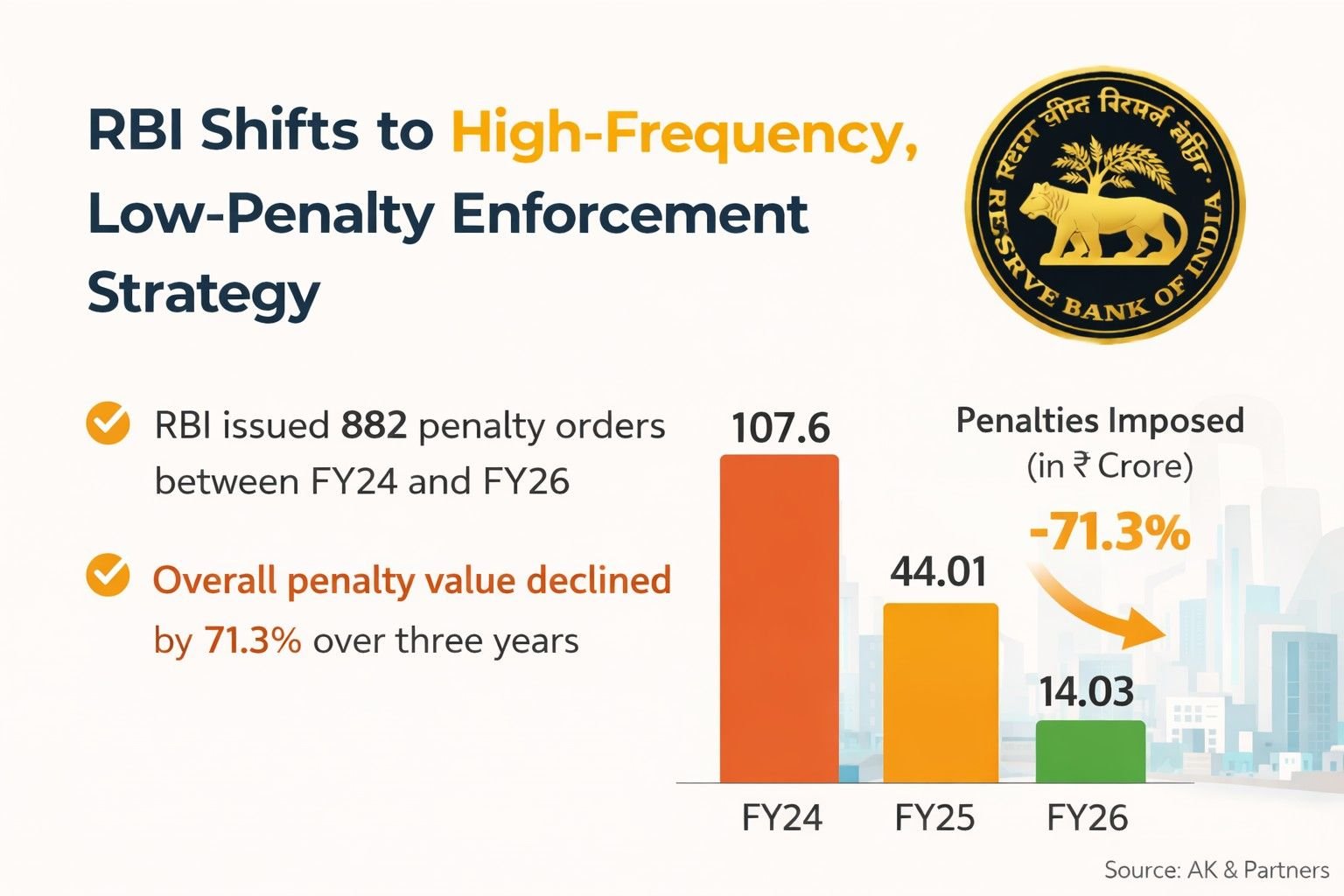

Decline in Penalty Amount, Not Enforcement

According to a report by AK & Partners:

- RBI issued 882 penalty orders between FY24 and FY26

- Total penalties amounted to around ₹166 crore

- Overall penalty value declined by 71.3% over three years

Year-wise Data:

- FY24: 305 orders → ₹87.40 crore

- FY25: 333 orders → ₹53.92 crore

- FY26: 245 orders → ₹25.07 crore

Despite the fall in penalty amounts, enforcement activity remained high, indicating redistribution—not reduction—of regulatory intensity.

Shift in Enforcement Strategy

A key trend is the move from large penalties to repeated smaller actions:

- Over 90% of penalties now fall below ₹1 crore

- Strong clustering under ₹50 lakh

- High-value penalties (above ₹1 crore) have nearly disappeared

This approach aims to:

- Ensure continuous monitoring

- Drive behavioural correction

- Prevent violations at an early stage

Focus Areas of RBI Supervision

1. Commercial Banks

- FY26 shows increased focus on commercial banks

- Larger institutions face greater regulatory scrutiny due to systemic importance

2. NBFCs

- Enforcement orders:

- FY24: 27 → FY25: 48 → FY26: 31

- Penalties sharply declined:

- ₹12.41 crore → ₹7.48 crore → ₹1.8 crore

- Average penalty reduced to ~₹5.8 lakh per order

This indicates earlier intervention and continuous supervision.

3. Cooperative Banks

- Account for 70–75% of total enforcement cases

- But contribute only 15–26% of total penalty value

4. Banks (Public & Private)

- Private banks: penalties down 67.3%

- Public sector banks: penalties down 58.8%

- Typical penalty range: ₹10 lakh – ₹75 lakh

5. Payment Entities

- Shift from large one-time penalties to multiple smaller penalties

- Example:

- FY24: One penalty above ₹5 crore

- FY26: Five penalties totaling ₹0.89 crore

Rising Use of Stronger Deterrents

- Cancellation of licenses is emerging as a more powerful enforcement tool

- Registration cancellations increased:

- 167 (FY24) → 181 (FY26)

Common Violations

Across all entities, the most frequent violations include:

- KYC non-compliance

- Breach of exposure norms

- Loans to directors/related parties

- Deposit-related violations

- Interest rate irregularities

Geographical Trends

- Maharashtra emerged as the top enforcement hub

- Accounted for:

- 288+ penalties

- ₹73.58 crore in fines

- Increasing cases related to loan and advance irregularities

Future Outlook

RBI’s enforcement focus is expected to shift towards:

- Digital lending risks

- Cybersecurity resilience

- Outsourcing and fintech partnerships

Conclusion

The RBI’s evolving strategy signals a clear shift from “high penalties, low frequency” to “low penalties, high frequency.”

This model emphasizes:

- Continuous compliance

- Early detection of risks

- Sustained regulatory engagement

For financial institutions, this means compliance is no longer occasional—it must be consistent, proactive, and deeply embedded in operations.