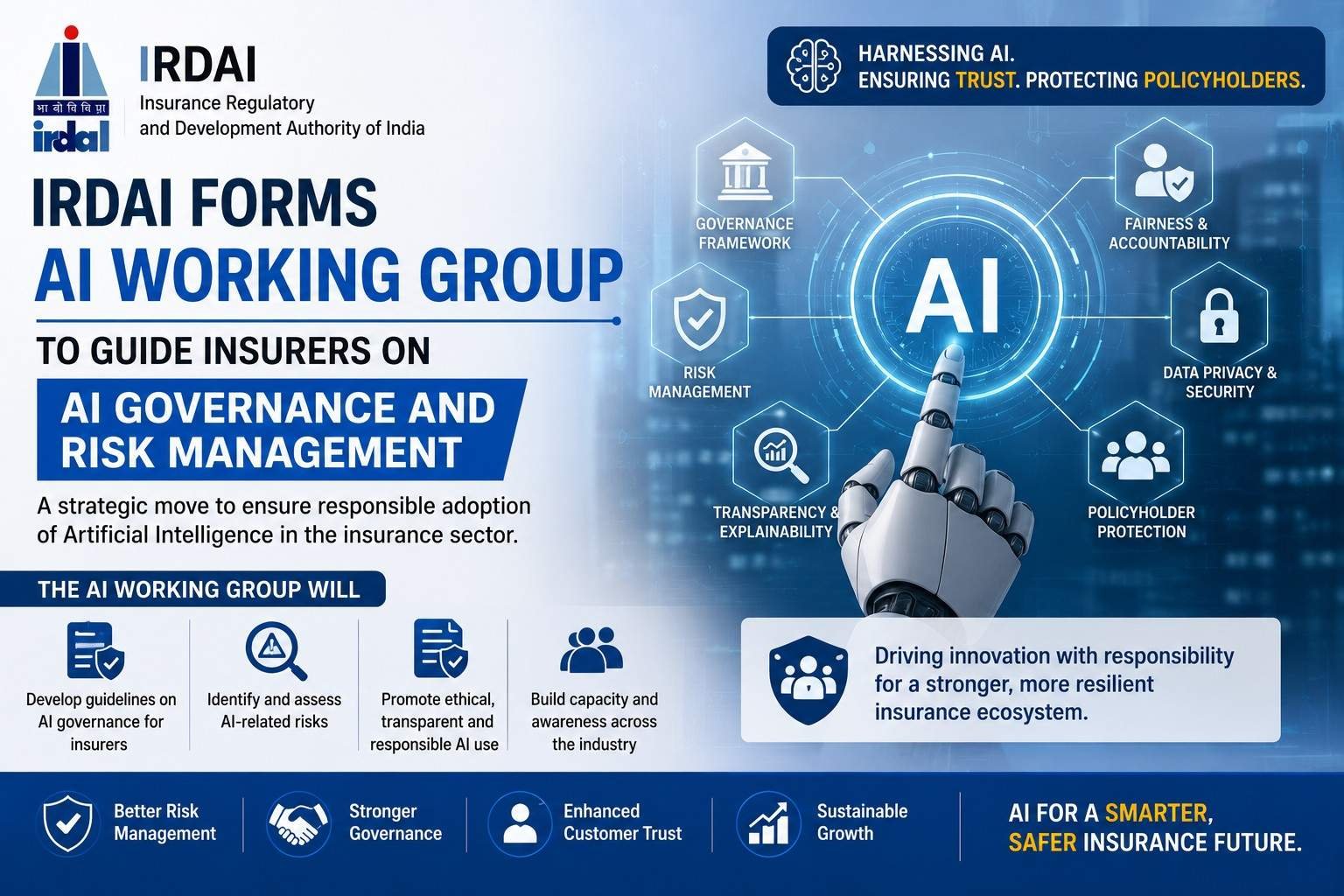

- The Insurance Regulatory and Development Authority of India (IRDAI) has constituted a dedicated working group on Artificial Intelligence (AI) to guide insurance companies on the responsible adoption, governance, and oversight of AI technologies.

- The move comes as insurers increasingly deploy AI-based solutions in underwriting, claims processing, customer service, fraud detection, and risk assessment.

Why Has IRDAI Formed the AI Working Group?

The insurance regulator noted that rapid advancements in artificial intelligence are transforming the insurance industry.

While AI offers:

- Faster claims processing.

- Better customer experience.

- Improved risk assessment.

- Fraud detection capabilities.

- Operational efficiency.

It also introduces several risks, including:

- Data privacy concerns.

- Cybersecurity threats.

- Ethical issues.

- Bias in algorithms.

- Operational risks.

IRDAI believes that insurers must adopt AI responsibly while protecting policyholders’ interests.

Who Will Head the AI Working Group?

The committee will be chaired by:

Prof Sandeep K Shukla

He currently serves as the Director of:

International Institute of Information Technology Hyderabad

The expert panel will study the impact of AI technologies on the insurance ecosystem and recommend appropriate governance frameworks.

Key Objectives of the AI Working Group

The working group will focus on:

1. AI Governance Framework

Developing guidelines for:

- Responsible AI use.

- Transparency.

- Accountability.

- Ethical practices.

2. Risk Management

Addressing risks related to:

- Algorithmic bias.

- Operational failures.

- Model risks.

- Cyber threats.

3. Policyholder Protection

Ensuring:

- Data privacy.

- Customer consent.

- Fair treatment.

- Secure handling of personal information.

4. Best Practices

Recommending industry-wide standards for AI implementation.

Why AI Matters for Insurance Companies

Insurance companies are increasingly using AI for:

- Claims settlement.

- Customer support chatbots.

- Fraud detection.

- Risk pricing.

- Underwriting.

- Document verification.

- Personalized products.

AI can reduce costs and improve efficiency, but regulators want to ensure that technology does not compromise fairness and consumer rights.

IRDAI’s Concern Over Cybersecurity

The regulator stated that emerging technologies are reshaping the cybersecurity landscape.

Potential concerns include:

- Data breaches.

- Unauthorized access.

- AI-driven fraud.

- Manipulation of models.

- Privacy violations.

The working group is expected to recommend safeguards to minimize these risks.

Proposed New Regulations for 2026

IRDAI has also released an exposure draft proposing:

IRDAI (Procedure for Making Regulations and Subsidiary Instructions) Regulations, 2026

The proposed regulations are being introduced under:

Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025

Major Features of the Proposed Regulations

Public Consultation Framework

IRDAI proposes wider consultation before introducing regulations.

Economic Impact Analysis

The regulator may:

- Assess costs.

- Analyze benefits.

- Evaluate industry impact.

Expert Consultation

The authority may establish specialized committees to provide domain expertise.

Insurance Advisory Committee

The proposed framework continues consultation with the Insurance Advisory Committee under the:

Insurance Regulatory and Development Authority Act, 1999

Impact on the Insurance Industry

The new AI framework could:

- Improve trust in AI systems.

- Strengthen customer protection.

- Enhance cybersecurity standards.

- Promote responsible innovation.

- Encourage ethical AI adoption.

Insurance companies may soon need to establish:

- AI governance policies.

- Internal monitoring mechanisms.

- Risk management systems.

- Data protection frameworks.