In a major policy shift aimed at strengthening borrower protection during crises, the Reserve Bank of India (RBI) has introduced a revamped framework for handling loans impacted by natural disasters and external disruptions. The updated guidelines are designed to ensure faster relief, improve transparency, and enable banks to respond proactively when borrowers face financial stress due to unforeseen calamities.

This move is part of the “Resolution of Accounts Impacted by Calamities” under the Reserve Bank of India (Commercial Banks – Resolution of Stressed Assets) Second Amendment Directions, 2026.

Why RBI Updated the Framework

India is highly vulnerable to natural disasters such as floods, cyclones, and earthquakes. In addition, events like riots or civil disturbances can disrupt economic activity and severely impact borrowers’ repayment capacity.

The earlier framework often led to delays in relief measures, primarily because banks waited for borrower requests or lacked clear timelines. Recognizing these gaps, the RBI has now introduced a time-bound and structured approach to ensure immediate financial assistance.

What Qualifies as a “Calamity”?

Under the revised norms, a “calamity” includes:

- Natural disasters like floods, earthquakes, cyclones

- Events officially recognized under disaster relief frameworks such as:

- National Disaster Response Fund (NDRF)

- State Disaster Response Fund (SDRF)

- External disruptions like riots or civil disturbances affecting economic activity

This broader definition ensures that more affected borrowers can access relief.

Key Eligibility Criteria for Borrowers

The RBI has clearly defined who can benefit from this framework:

- The loan account must be classified as ‘Standard’

- The borrower should not be overdue by more than 30 days at the time of the calamity

- Financial stress must be directly linked to the disaster event

This ensures that relief is targeted at genuinely impacted borrowers, not those already in deep financial distress.

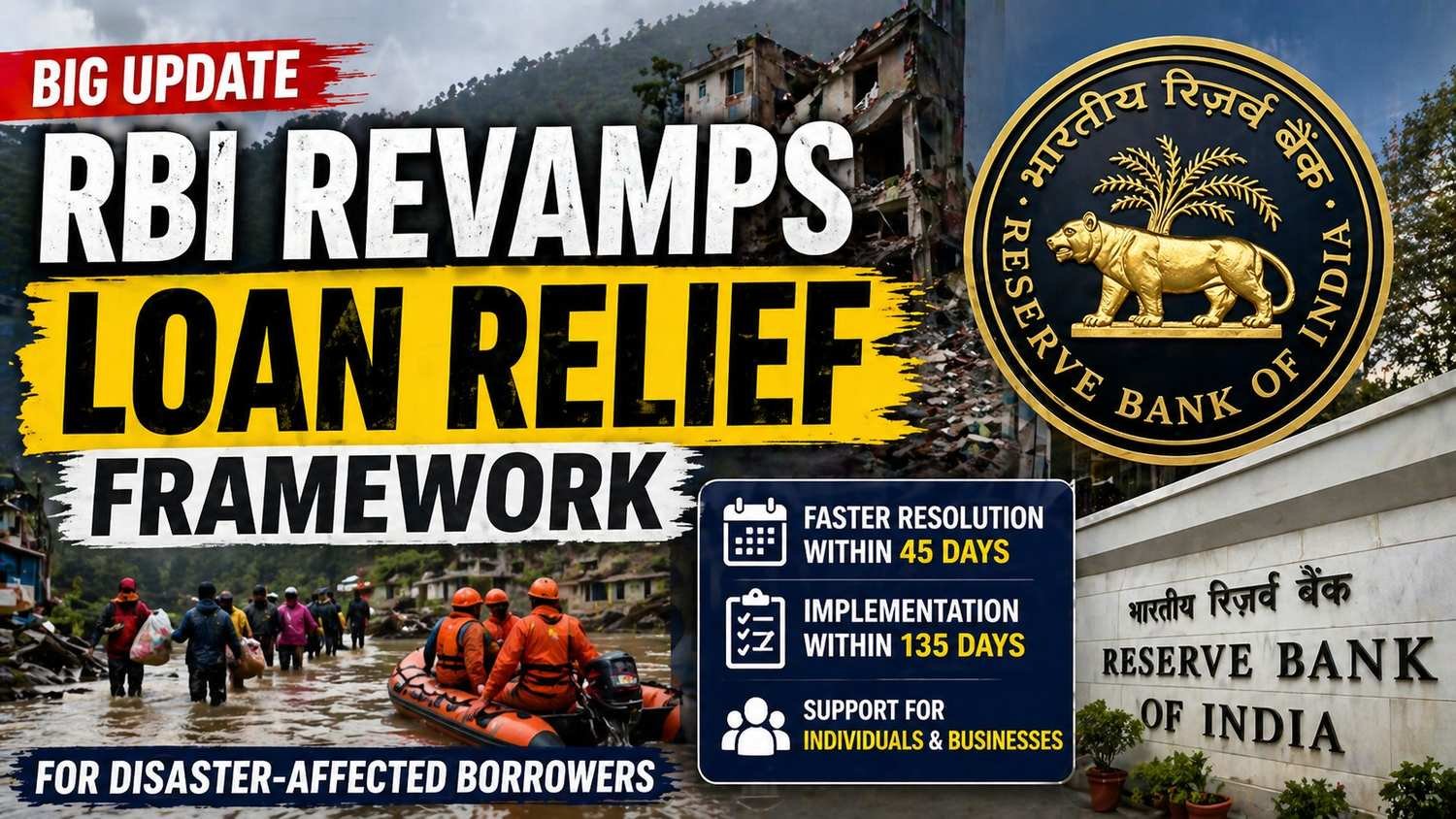

Strict Timelines: Faster Relief Than Before

One of the most impactful changes is the introduction of mandatory timelines:

- Resolution plan must be invoked within 45 days of calamity declaration

- Implementation must be completed within 135 days

These deadlines ensure that banks act quickly, preventing prolonged financial uncertainty for borrowers.

Banks Can Now Act Without Waiting for Requests

A significant shift in the new framework is that banks are now allowed to initiate restructuring proactively.

Earlier, borrowers had to formally apply for relief, which often delayed the process. Now, banks can act based on recommendations from:

- State Level Bankers’ Committees (SLBCs)

- Union Territory Level Bankers’ Committees (UTLBCs)

- District Consultative Committees (DCCs)

However, borrower autonomy is still protected—customers have the right to opt out of the restructuring plan within the implementation period.

Types of Relief Measures Offered

The RBI has given banks flexibility to design relief packages depending on the borrower’s financial condition and viability. Some key measures include:

1. Rescheduling of Loan Repayments

Borrowers may get extended timelines to repay their loans, easing immediate financial pressure.

2. Conversion of Interest into Credit Facility

Accrued interest can be converted into a separate loan, reducing the repayment burden in the short term.

3. Moratorium or Payment Relief

Temporary relief on EMIs can be provided during the recovery phase.

4. Loan Tenure Extension

Banks may increase the loan tenure to make repayments more manageable.

All these measures are subject to the viability assessment of the borrower, ensuring sustainability.

Integration with Insurance and Government Schemes

The RBI has emphasized a holistic approach to financial relief:

- Insurance claims must be considered while restructuring loans

- Banks should align their relief measures with government schemes, such as:

- Interest subvention programs

- Disaster relief assistance initiatives

This ensures that borrowers receive maximum possible support from multiple channels.

Mandatory Internal Policies for Banks

To enhance consistency and accountability, the RBI has made it compulsory for banks to develop detailed internal frameworks, covering:

- Eligibility conditions

- Types of restructuring options

- Approval mechanisms

- Monitoring and reporting systems

This will reduce ambiguity and ensure uniform implementation across banks.

Conclusion:

The RBI’s revamped guidelines represent a major reform in India’s banking sector, especially in the context of disaster management and financial inclusion. By introducing clear timelines, proactive intervention, and borrower-friendly provisions, the central bank has ensured that financial institutions are better equipped to handle crisis situations.

If implemented effectively, this framework will not only support borrowers during tough times but also strengthen the resilience of India’s banking system in the face of increasing environmental and economic uncertainties.