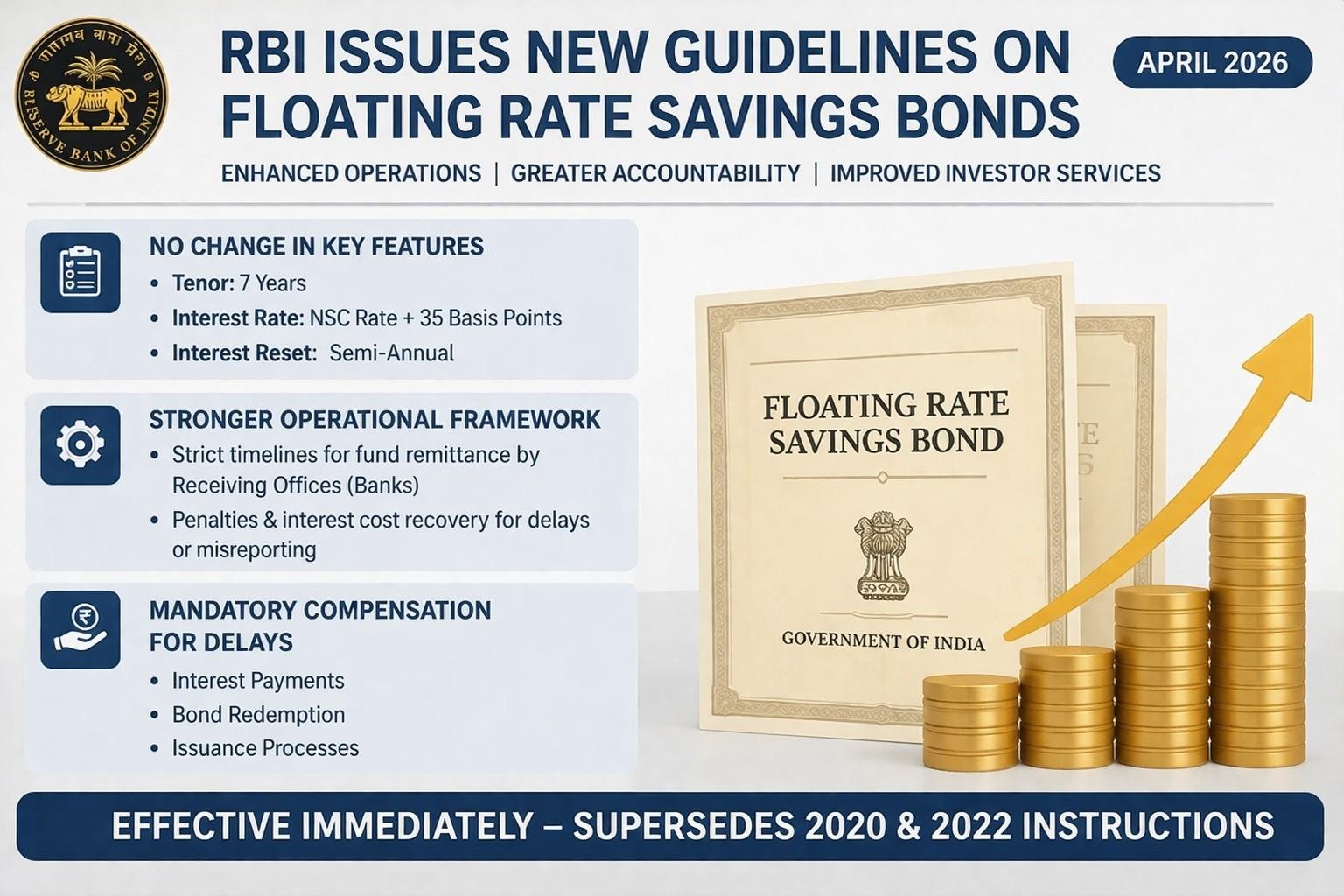

The Reserve Bank of India has issued a new circular in April 2026 on Floating Rate Savings Bonds, retaining the core structure of the product while introducing major improvements in its operational framework.

The revised guidelines aim to enhance digitisation, accountability, and investor service standards, and have come into effect immediately, replacing earlier instructions issued in 2020 and updated in 2022.

No Change in Key Features

The RBI has kept the fundamental structure of the bonds unchanged:

- Tenor: 7 years

- Interest Rate: Linked to National Savings Certificate (NSC) rate + 35 basis points

- Interest Reset: Semi-annual

This ensures continuity for investors while maintaining alignment with prevailing small savings rates.

Stronger Operational Framework

The new guidelines significantly revamp the operational processes:

- Banks acting as Receiving Offices (ROs) must follow strict timelines for fund remittance

- Penalties and interest cost recovery will apply in cases of delays or misreporting

- Mandatory compensation to investors for delays in:

- Interest payments

- Bond redemption

- Issuance processes

Improved Transparency with Structured Nomination

To enhance clarity for investors, RBI has introduced:

- Structured nomination system

- Amount-wise allocation among nominees

This move is expected to reduce disputes and improve transparency in fund distribution.

Push for Digital Access

A key highlight of the circular is the focus on digitisation:

- Receiving offices must provide online application facilities

- Deadline for implementation: September 30, 2026

- Improved account visibility and servicing standards

This aligns with the broader push towards digital financial services in India.

Enhanced Compliance Requirements

The RBI has also strengthened regulatory compliance norms:

- Mandatory PAN submission as per updated tax rules

- Reporting under Statement of Financial Transactions (SFT)

- Alignment with the Digital Personal Data Protection (DPDP) framework

These measures aim to ensure better transparency, data security, and regulatory oversight.

Conclusion

The RBI’s updated framework for Floating Rate Savings Bonds strikes a balance between stability and reform. While the core investment features remain unchanged, the enhanced operational and digital measures are expected to improve efficiency, investor protection, and service quality.