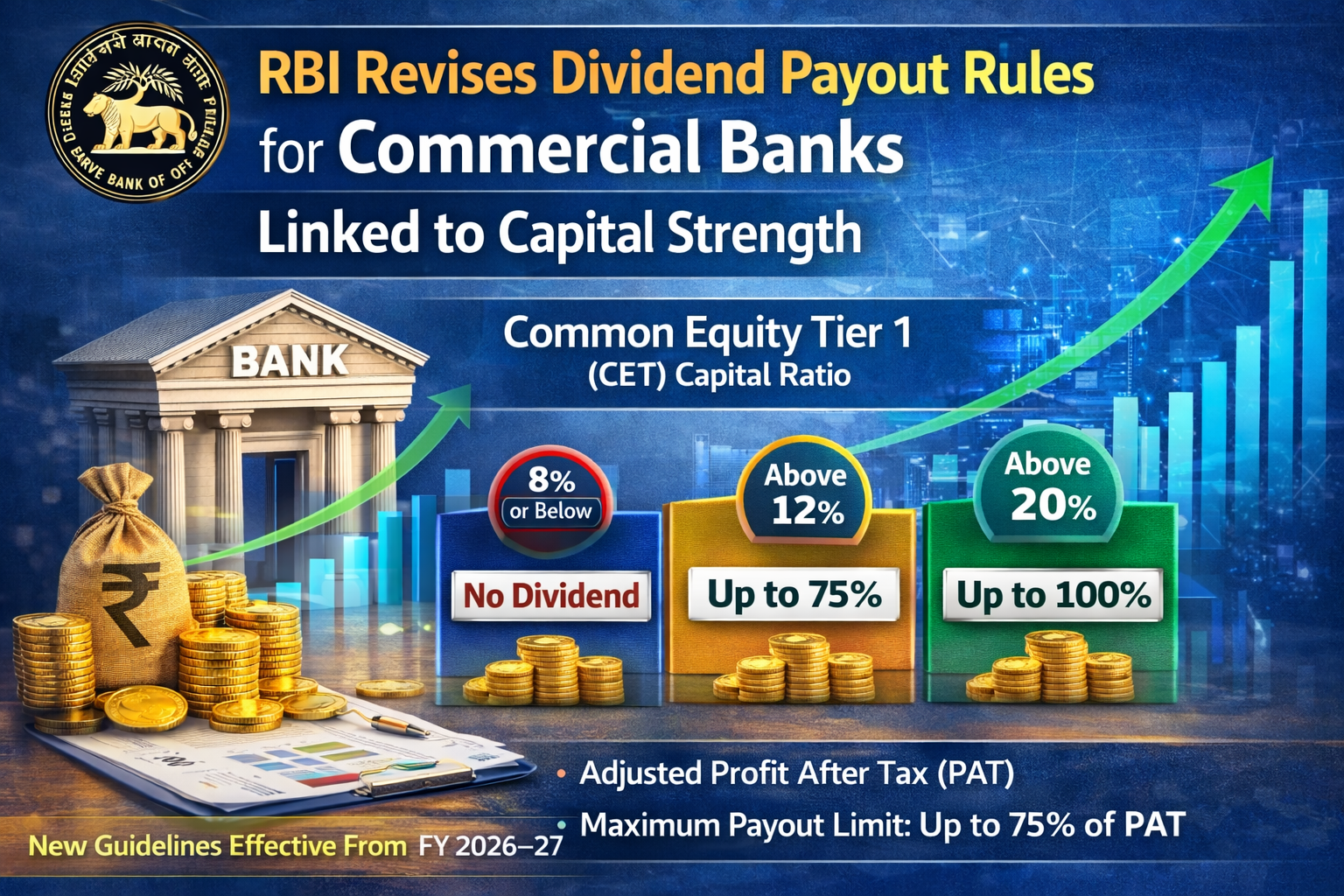

The Reserve Bank of India (RBI) has introduced revised prudential norms for dividend payouts by commercial banks, linking them directly to their Common Equity Tier 1 (CET1) capital ratios. The new rules replace the earlier guidelines issued in November 2025 and will come into effect from financial year 2026–27 (FY27).

The updated framework, titled “Reserve Bank of India (Commercial Banks – Prudential Norms on Declaration of Dividend and Remittances of Profits) Directions, 2026,” aims to ensure that banks maintain strong capital buffers before distributing profits to shareholders.

Dividend Payout Linked to Capital Strength

Under the revised framework introduced by the Reserve Bank of India, banks will be placed into 10 different capital-ratio buckets based on their CET1 ratio.

-

Banks with a CET1 ratio of 8% or below will not be allowed to declare any dividend.

-

Banks with a CET1 ratio above 20% fall in the highest category and may distribute up to 100% of their adjusted profit after tax (PAT) as dividends.

However, the RBI has imposed an additional safeguard:

Total dividend payouts cannot exceed 75% of a bank’s profit after tax for the financial year, regardless of the capital bucket in which the bank falls.

Introduction of “Adjusted Profit After Tax”

A key feature of the new rules is the introduction of “Adjusted PAT.”

Adjusted PAT is calculated as:

Net Profit – 50% of Net Non-Performing Assets (NPAs) as of March 31 of the relevant financial year.

This mechanism effectively reduces the dividend-paying capacity of banks with higher bad loan burdens, encouraging them to focus on improving asset quality before distributing profits.

Additional Rules for Systemically Important Banks

Banks classified as Domestically Systemically Important Banks will face stricter conditions.

For these banks, the D-SIB capital buffer requirement will be added to each CET1 threshold, making it more difficult for them to qualify for higher dividend payout categories. This measure ensures that large and systemically important banks maintain stronger capital protection.

Conditions for Declaring Dividends

To declare dividends under the new framework, banks must satisfy several conditions:

-

Maintain the required regulatory capital levels before and after dividend distribution

-

Report a positive Adjusted PAT

-

Ensure that there are no restrictions imposed by RBI on dividend distribution

These rules are designed to ensure that dividend payments do not weaken a bank’s financial stability.

Role of the Bank’s Board of Directors

The board of directors of a bank must carefully evaluate several factors before approving dividend payments, including:

-

Any divergence in asset classification and NPA provisioning identified during RBI supervision

-

Auditors’ reports, including modified opinions or emphasis of matter

-

The bank’s current and projected capital position

-

Long-term growth and expansion plans

This ensures that dividend decisions are made after considering the bank’s overall financial health.

Rules for Foreign Banks in India

Foreign banks operating in India through branch offices will be allowed to remit their net profits to their head offices without prior approval from the RBI, provided their financial accounts are audited.

However, certain items cannot be included in remittable profits, such as:

-

Exceptional or extraordinary income

-

Profits overstated by auditors

-

Unrealised gains from Level 3 financial instruments

Reporting Requirement

Banks must inform the RBI’s Department of Supervision within two weeks of declaring dividends or remitting profits.

Failure to comply with these guidelines may lead to supervisory or enforcement action by the central bank.

Objective of the New Framework

Through these revised prudential norms, the Reserve Bank of India aims to strike a balance between rewarding shareholders and ensuring the financial stability of banks. By linking dividend payouts to capital strength and asset quality, the RBI seeks to encourage banks to maintain stronger balance sheets and better risk management practices.